Table of Contents

- What CrossMarket AI Claims To Be

- The Promise Of “Stable Daily Returns”

- How The Platform Feels To Use

- Product Snapshot: Claims vs Visible Reality

- The “AI” Story That Never Becomes Concrete

- Ownership, Background, And Structural Opacity

- The Referral Engine And Network‑Marketing Dynamics

- Risk Snapshot: Structural Warning Signs

- Trust, Security, And The Withdrawal Problem

- When The Numbers Break The Story

- Real User Reviews: What Trustpilot Shows

- Comparison With Legitimate Cross‑Market And AI Tools

- Overall Verdict

CrossMarket AI looks impressive at first glance, sleek dashboards, bold claims of AI‑driven arbitrage, and the promise of daily passive income but when you look closely at how it works, how it is structured, and what it asks you to believe, it starts to resemble a high‑risk HYIP‑style scheme much more than a serious AI trading product.

What CrossMarket AI Claims To Be

CrossMarket AI (often presented as Crossmarket.ai or Cross Market AI) is introduced as an automated crypto arbitrage platform powered by advanced artificial intelligence. It claims to scan multiple cryptocurrency exchanges in real time, identify tiny price differences on the same asset, and automatically execute buy‑low / sell‑high trades to generate “small but steady” gains for users.

The branding leans heavily on language like “emotion‑free trading,” “24/7 AI monitoring,” and “stable daily returns,” creating the impression of institutional‑grade technology wrapped in a consumer‑friendly interface. The typical flow is simple: sign up, deposit crypto or stablecoins, select an AI plan, and then mostly watch the numbers on a dashboard change. Very little is discussed about order books, spreads, or detailed strategy logic, which makes the product feel accessible even to people with no trading background.

To someone new, this narrative can feel reassuring. The platform positions itself as the intelligent middleman: it deals with market complexity while you simply provide capital and wait for results.

The Promise Of “Stable Daily Returns”

At the centre of the marketing and word‑of‑mouth pitch is the idea of “fixed” or “stable” daily returns, often framed in the 0.5–1% per‑day range. This is described as achievable because the system supposedly focuses on arbitrage rather than speculation. Arbitrage is presented as market‑neutral: instead of guessing whether a coin will rise or fall, the system claims to profit from price gaps between exchanges.

This story is powerful because it speaks to two strong desires: avoiding emotional trading mistakes and enjoying consistent passive income. Dashboards and promotional screenshots showing balances creeping up each day reinforce the idea that the money is “working” continuously in the background, without the user needing to make decisions or handle volatility.

However, there is no independently audited performance history behind these promises. There are no neutral third‑party verifications or publicly verifiable track records just the internal numbers displayed on the platform and testimonials that depend on them. In practice, users are asked to accept the platform’s self‑reported profitability without external proof.

How The Platform Feels To Use

Onboarding follows a familiar pattern. New users create an account with an email and password, sometimes complete a basic identity check, and are then strongly encouraged to deposit funds or connect wallets. Once funds arrive, the platform guides them toward choosing or activating an AI strategy, often framed as a recommended or default option.

After that point, the experience becomes largely passive. The dashboard takes centre stage, showing:

● Overall account balance

● Daily and cumulative “profit”

● Bot or strategy status (running/paused)

● High‑level metrics like “AI success rate” or “market opportunities identified”

The design is smooth and deliberately reassuring. Numbers are presented clearly, with tidy charts and calm colours. For many users, watching the balance rise over days or weeks feels like confirmation that the system is doing exactly what it promises.

Yet beneath that surface, there is very little visibility into the internal mechanics. Which exchanges are actually connected? How large are the trades? How are fees and slippage accounted for? How is risk controlled during volatile market periods? Answers to these questions are either absent or extremely vague. In essence, funds go in, outputs appear on the screen, and the process in between remains a black box.

Product Snapshot: Claims vs Visible Reality

A simple way to see the gap is to lay out the key product promises against what is actually observable from the outside:

| Aspect | What CrossMarket AI Promises | What Is Actually Visible To Users |

| Core function | AI‑driven arbitrage across multiple exchanges | Dashboard numbers and generic “AI” messaging |

| Daily returns | Around 0.5–1% “stable” profit per day | Internal profit figures, no audited performance |

| Risk profile | Market‑neutral, “low‑risk” due to arbitrage | No transparent risk disclosures or stress‑test data |

| User involvement | Set‑and‑forget automation | Minimal control, minimal visibility into strategy |

| Technical detail | Advanced AI and cross‑market correlation analysis | No real whitepaper, no public model or strategy overview |

| Legal / compliance | Implied safety through professional branding | Opaque ownership, no clear major regulatory registration |

This contrast sets the tone for the rest of the assessment.

The “AI” Story That Never Becomes Concrete

The platform’s main selling point is its supposed artificial intelligence, yet the supporting detail rarely goes beyond marketing language. Common phrases include “cross‑market correlation analysis,” “multi‑exchange arbitrage engine,” and “intelligent risk control,” but there is no publicly available technical whitepaper that explains:

● What data is ingested and at what frequency

● Which exchanges are connected and how latency is managed

● What types of models are used (e.g., statistical arbitrage, machine learning classifiers, reinforcement learning)

● How fees, slippage, and liquidity constraints are handled

● How positions are sized and risk is capped

In serious algorithmic trading environments, even when code is proprietary, there is usually at least a high‑level description of strategy types, constraints, and limitations. Here, the emphasis is on AI as a label to inspire confidence rather than as a system whose behaviour can be meaningfully evaluated.

This gap between language and substance sits uncomfortably close to what regulators and analysts now describe as “AI washing” using AI terminology to make speculative or unrealistic financial promises sound more convincing.

Ownership, Background, And Structural Opacity

When attention shifts from the product to the people and entities behind it, another layer of concern appears. Ownership details are obscured behind privacy services, company structures are not clearly explained, and there is no prominent, accountable team presented in the way reputable financial platforms usually do.

This lack of transparency is notable in a space where trust depends heavily on knowing who holds user funds and who is responsible when things go wrong. In regulated markets, founders, executives, and legal entities are visible and subject to oversight. Here, those elements largely remain out of view.

The broader landscape of similarly named and similarly structured platforms adds context: repeated rebranding, aggressive marketing, and sudden shutdowns have been common patterns in high‑yield schemes. When a new product appears with strong promises, opaque ownership, and heavy emphasis on recruitment, it naturally inherits some of that suspicion.

The Referral Engine And Network‑Marketing Dynamics

CrossMarket AI does not only rely on its own website or advertising. A large part of its growth has come through referrals and network‑style promotion. People often hear about it from acquaintances, community leaders, or online promoters who receive financial incentives for bringing in new participants.

The referral structure is typically more complex than a simple one‑time bonus. It can involve multi‑tier commissions, where rewards are tied not only to direct invites but also to the activity of those invitees’ networks. This creates strong incentives to:

● Share profit screenshots

● Publicly celebrate returns

● Encourage others to sign up quickly

● Downplay or ignore early warning signs

For a period, this can create a self‑reinforcing loop: as long as new money enters and dashboards show profits, enthusiasm remains high. At the same time, the reliance on constant recruitment begins to resemble the payout dynamics of pyramid‑style schemes, especially when there is no verifiable trading profit underpinning the system.

Risk Snapshot: Structural Warning Signs

From a risk‑analysis perspective, several structural elements stand out:

| Category | Observed Pattern | Why It Matters |

| Ownership | Anonymous or hard‑to‑trace principals | Limits accountability and legal recourse |

| Regulation | No clear registration with major financial authorities | Users lack formal investor protections |

| Custody | Platform holds or effectively controls user funds | Single point of failure and counterparty risk |

| Transparency | No audited performance, no detailed trading statements | Claims cannot be independently verified |

| Growth model | Heavy emphasis on referrals and team building | Suggests dependency on new deposits for sustainability |

| Communication | Strong marketing, weak technical and risk disclosures | Imbalance between sales messaging and substance |

Each item on its own would warrant caution; taken together, they form a dense cluster of red flags.

Trust, Security, And The Withdrawal Problem

A recurring pattern across high‑risk platforms is the difference between how easy it is to deposit and how hard it can become to withdraw. With CrossMarket AI, stories commonly follow this progression:

1. Initial deposits are processed smoothly.

2. Early, small withdrawals are sometimes honoured, which builds confidence.

3. Over time, as balances grow and more users attempt to withdraw, delays and complications become more frequent.

4. Explanations often reference “technical maintenance,” “security checks,” or “compliance reviews.”

5. In some cases, withdrawals are partially released or blocked altogether.

Parallel to this behavioural pattern, independent risk‑checking tools often flag domains with similar characteristics: young age, hidden ownership, and certain technical signals as high‑risk or potentially unsafe. That implies that risks are not limited to losing deposited funds; personal data, identity documents, and login credentials could also be exposed to misuse.

When a platform combines opaque ownership, custody of funds, and increasing friction on withdrawals, the practical risk profile moves far away from ordinary market risk and towards platform‑failure or fraud risk.

When The Numbers Break The Story

One of the simplest and most powerful ways to test CrossMarket AI’s narrative is to apply basic math. At 1% per day, even modest capital grows extraordinarily fast if returns are compounded. For example, under ideal conditions:

● 1% per day for 30 days implies roughly a 35% increase

● Over a year, the growth becomes exponential and unrealistic at any meaningful scale

Real markets do not leave such low‑risk, high‑return opportunities unexploited, especially not in highly monitored and competitive areas like exchange arbitrage. Professional trading firms with advanced infrastructure aggressively pursue small edges; persistent, scalable, low‑risk returns of this magnitude would attract huge capital and quickly shrink spreads.

By claiming that such returns are routinely available to large numbers of retail users through a simple web interface, without clear strategy disclosure or independent audits, the platform asks users to accept an economic story that conflicts with how markets actually behave.

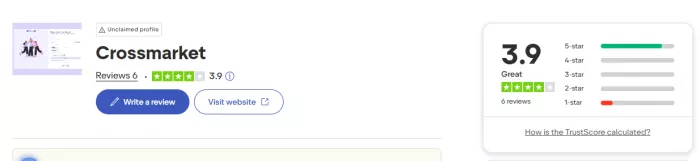

Real User Reviews: What Trustpilot Shows

One of the clearest ways to understand CrossMarket AI’s real-world performance is through its Trustpilot page. At first glance, the platform appears fairly rated, with an average score of around 3.8 out of 5 based on just 5–6 reviews. While this may seem acceptable, such a small number of reviews makes the rating unreliable and not very meaningful.

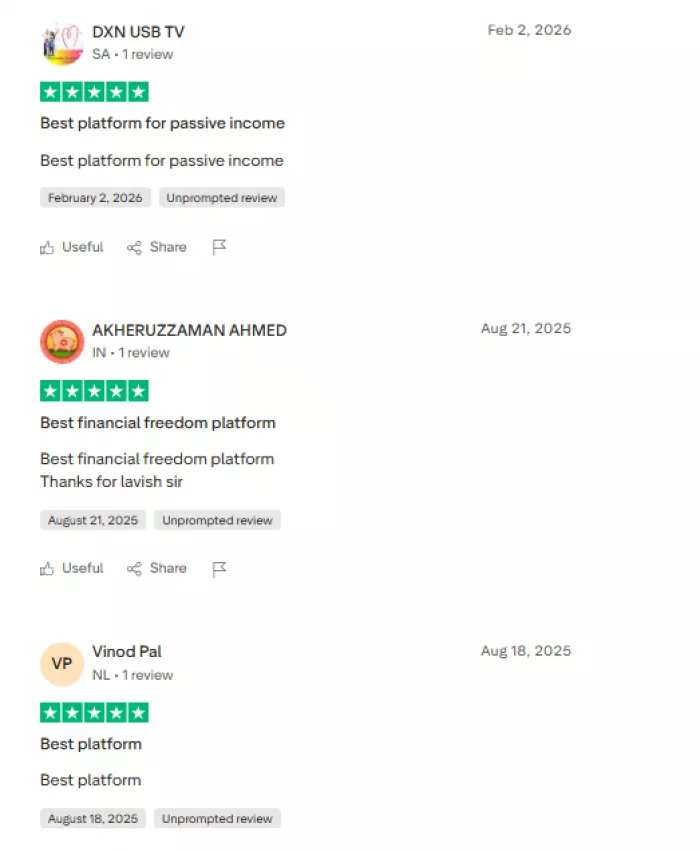

Most of the 5-star reviews are very brief and sound promotional rather than genuine. Comments like “Best platform” or “Great opportunity for passive income” lack important details such as user experience, duration of use, investment amounts, or proof of withdrawals. Many even repeat similar phrases and mention the same individual, which raises concerns about authenticity.

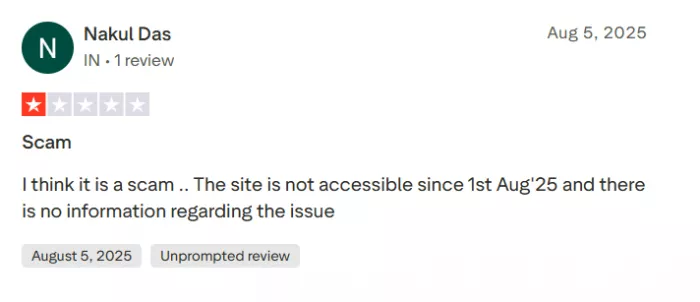

In contrast, the single 1-star review is detailed and concerning. It claims the platform became inaccessible around August 1, 2025, with no communication from the company regarding user funds. This aligns with common warning signs seen in questionable platforms, where operations suddenly stop without explanation.

Overall, due to the very limited number of reviews and the suspicious pattern of overly positive feedback mixed with a serious negative report, the Trustpilot rating should not be taken as proof of legitimacy. Instead, it may serve as an early warning sign requiring further caution.

Comparison With Legitimate Cross‑Market And AI Tools

In contrast to this model, there are legitimate cross‑market analytics and AI‑driven tools in the financial ecosystem. These typically share several characteristics:

● They focus on providing data, analytics, and signals, not on directly holding user funds.

● They integrate with recognised brokers or exchanges, often through APIs.

● They disclose the core team, maintain a public track record, and sometimes publish research or documentation.

● They may operate under regulatory frameworks or undergo external security audits.

● Users retain control over execution and custody, choosing how to act on the insights provided.

CrossMarket AI diverges from this pattern in important ways. It wants control or at least effective control of user funds, provides minimal visibility into strategies, offers no meaningful third‑party verification of performance, and does not present a clear regulatory footprint. For anyone familiar with genuine institutional or professional‑grade tools, that contrast is telling.

Overall Verdict

Looked at in isolation, any single feature of CrossMarket AI, the polished interface, the AI branding, the attractive daily return figure might appear compelling. Taken together with the platform’s structural opacity, referral‑heavy growth model, lack of verifiable performance data, custody of user funds, and withdrawal‑related concerns, the overall risk profile is extremely high.

The central tension is simple: a service that truly delivered low‑risk, high, stable arbitrage returns at scale would not need opaque ownership, aggressive recruitment incentives, or vague technical explanations. The fact that all of those elements are present here suggests that the primary story is not about sophisticated AI trading, but about extracting value from user deposits and networks.

For anyone considering involvement, the cautious conclusion is clear. If the goal is to explore algorithmic or AI‑assisted trading, there are safer approaches that keep custody on regulated exchanges or with licensed brokers, use reputable analytics tools, and avoid platforms that promise daily passive profits with minimal transparency. In this context, participation in CrossMarket AI looks less like prudent investing and more like speculation on the continued functioning of a fragile, opaque scheme.

Comments